1. Introduction

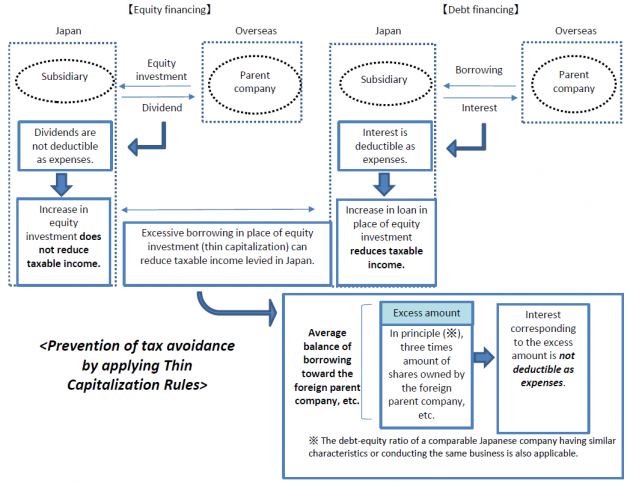

Japanese subsidiaries and branches of foreign companies (foreign-owned companies) can raise financing in the form of equity investment or borrowing from their parent company. While dividends on equity investment are not tax-deductible, interest is deductible as expenses and can reduce taxable income of foreign-owned companies.

Thin capitalization rules are aimed at preventing tax avoidance caused by increasing interest on excessive borrowing from foreign related companies. The interest expenses corresponding to the excess amount of debt over the safe-harbor of the debt-equity ratio are disallowed in computing corporation tax of foreign-owned companies.

2. Thin capitalization rules

Thin capitalization rules are stipulated in Article 66-5 “Special Rules of Interest on Indebtedness Pertaining to Foreign Controlling Shareholders, etc.” under Special Taxation Measures Law.

In cases where domestic companies pay interest on loans to foreign controlling shareholders or specified loan providers, etc. (“foreign controlling shareholders, etc.”) and the average balance of interest-bearing debt exceeds three times of the net equity owned by the “foreign controlling shareholders, etc.,” the interest corresponding to such excess amount is not deductible as expenses.

3. Conclusion

In this News, we mentioned “Thin Capitalization Rules for Foreign-owned Companies.” Please note that this News only introduces general outlines and does not include professional advice. So please make sure not to make any decisions without taking professional advice individually. If you have any questions, please feel free to contact us.

(Reference / Japanese)

Ministry of Finance

Article 66-5 Special Taxation Measures Law

Cabinet Order 39-13 Special Taxation Measures Law

Query on the phone+81-3-6821-9455