1. Introduction

On 1 April, 2017, Payment Services Act, so called the Virtual Currency-Act was approved. In recent years, virtual currencies are getting more attention as convenient payment tools. However, virtual currencies did not have any clear statutory positions, and even regulations or guidance did not exist. Thus, virtual currencies were facing some problems such as international money laundering, terrorist funding, and users’ damage caused by bankruptcy of operators. From this background, opinions such as “Operators’ registration or licensing system should be set.” or “Identifying users and retaining transaction records should be considered. “ are now going up.

In this News, we will mention not only the enforcement of the Virtual Currency-Act but the consumption tax treatment and the basic knowledge of blockchain as virtual currencies’ core technology with its future possibilities.

2. Virtual-Currency Act ① Definition of Virtual Currencies

The Virtual Currency-Act defines virtual currencies as follows. It distinguishes virtual currencies from methods of payment like Prepaid Cards, etc.

(1) Asset-like values (limited to those items electronically recorded by electronic or other equipment and excluding Japanese currency, foreign currency, and currency-denominated assets; the same applies to the item below) usable as payment to indefinite parties for the cost of purchases or rent of items or receipt of services and which can be transferred by means of electronic data processing systems;

(2) Asset-like values that can be used in exchange with indefinite parties for those items described in the preceding item and which can be transferred by means of electronic data processing systems.

3. Virtual-Currency Act ② Legal regulations to virtual currency operators

Main legal points are as follows.

(1) Registration system of virtual currency operators

Under satisfying compliances or requirements for financial base, etc., virtual currency operators are required to register to the Prime Minister.

(2) Business restrictions on virtual currency operators

Virtual currency operators are required to segregate users’ property from virtual currency operators’ own property including virtual currencies. Virtual currency operators must be regularly audited by an audit firm, etc. and report the activities to auditors.

(3) Supervision to virtual currency operators

Virtual currency operators must prepare documents, submit reports with the attachment of audit reports and undergo on-the-spot investigation.

4. Consumption tax treatment

The consumption tax treatment on virtual currencies was also amended. Virtual currencies were treated as “transfer, etc. of taxable assets” and taxable (non-taxable for export transactions) for consumption tax purposes. However, FY2017 Tax Reform amended the virtual currency transactions as non-taxable.

Virtual currencies are now recognized as one of the methods of payment and included into non-taxable transactions.

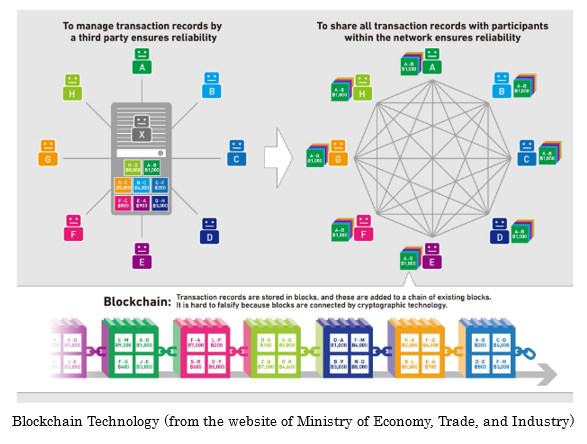

5. Blockchain technology

Virtual currencies’ core technology is blockchain. With the use of a peer to peer network, blockchain records transactions in a linear and chronological order by constantly building up recordings as blocks to be added with a new set of recordings. It is quite different from the conventional centralized database system. Blockchain technology, with its distributed information management structure, has the following characteristics:

① Blockchain maintains and shares data with all nodes participating in a system, which eliminates the risk of manipulating records or illegal transactions. Since copies of data in a blockchain are hosted by each user in a network, deleting such data is impossible.

② Blockchain enables direct trading among many unspecified users.

③ The old-style transactions were controlled by a trusted authority or a central server. Blockchain can eliminate such intermediates, and as a result, it can reduce management and maintenance costs.

6. Future trend

(1) Effects on general consumers

One major electric retailer announced that it adopted the experimental use of payment services by virtual currencies. Currently, credit cards are the most familiar means of payment except for cash. New regulations for virtual currencies will be expected to restore trust and accelerate trading volume in the future.

(2) Application of distributed management structure –Simplifying trading business

Blockchain technology is also applied to international business transactions.

In the conventional international trading, several parties from different countries intervene and make transactions more complicated. Further, use of letters of credit increases paper work, and sending letters or emails back and forth is disadvantageous in taking time.

Blockchain technology, with its distributed information management structure, enables several parties to share the information at the same time and can reduce time and cost significantly.

(3) Others

Blockchain is expected for its use in other fields such as investment, asset management, voting, and so on. The new technology will expand its possibilities in the future.

7. Conclusion

In this News, we have mentioned the Virtual Currency Act and blockchain as virtual currencies’ core technology. As is the case with the Internet, blockchain technology will have possibilities to make a big change in society.

Please note that this News only introduces general outlines and does not include professional advice. So please make sure not to make any decisions without taking professional advice individually. If you have any questions, please feel free to contact us.

Query on the phone+81-3-6821-9455